Friday, 29 August 2014

VIDEO: Why September is a Danger Month for Equities; but better for Bonds, NatGas, Gold...

Click below for a 3-minute Video Presentation on the Seasonal Dangers for Stocks,

Thursday, 28 August 2014

Blinkx, and You May Miss the Rebound!

What Does Blinkx Do?

The official blurb:

blinkx is an Internet media company that connects consumers and brands through premium content online. Founded in 2004, blinkx pioneered Internet Video Search using its patented COncept Recognition Engine (CORE). This technology leverages speech recognition, text and image analysis to deeply understand the meaning and context of video content to generate improved search relevancy for consumers and a brand safe environment for advertisers. Through its partnerships with hundreds of media companies, including NBC, Conde Nast, Reuters and Bloomberg, blinkx has indexed and search enabled millions of hours of video content. blinkx powers video search, discovery or monetization on thousands of online properties including Lycos, Discovery Networks, CBS and FoxSports. blinkx is headquartered in San Francisco, California with 15 offices worldwide.

Or, in the words of the website itself, it is:

A simple way to discover and share great videos.

Still confused as to what they do? Well, here is a link to a video demonstrating how to use the site:

What Is their Business Model?

London/San Francisco-headquartered Blinkx distributes ad-supported content, but has planted its flag firmly in video search and discovery. So it gets a cut of the advertising revenues.

Why has Blinkx Been Under Attack from Short Sellers?

This article on Bloomberg.com highlights a very critical blog post by a Harvard Business School professor, which triggered the stock’s biggest plunge ever.

In the Jan. 28 blog, entitled “The Darker Side of Blinkx", Benjamin Edelman, an associate professor of business administration, said his research indicated that the London-based company used deceptive software to inflate traffic counts and capture commissions. Edelman wrote that he prepared the research for an unnamed client.

At least 5 hedge fund short sellers have subsequently sold Blinkx short: the investment companies are Luxor Capital Group LP, Blau GmbH, Jericho Capital Asset Management LP, Valiant Capital Management LP and Oxford Asset Management LLP, according to European regulatory filings.

July 2 Profit Warning Underlines Problems at Blinkx

To add grist to the short sellers' mill, at the time of their trading statement on July 2, the company then issued a profit warning for H1 2015, highlighting lower-than-expected demand within their Desktop segment (as people increasingly access the internet via mobile devices rather than desktop PCs), hurting both sales and profits with full-year EBITDA some $5m below management's prior expectations.

The two volume spikes at the time of (a) the publication of the critical blog post at the end of January, and then (b) the profit warning at the beginning of July sent Blinkx's shares down from 217p in mid-January to 32p on July 2. By any stretch of the imagination, this made for an impressive return for anyone shorting the shares!

As a result of all this, one of the biggest investment banking cheerleaders for Blinkx, Goldman Sachs, waved the white flag and cut its analyst rating on Blinkx on July 7 from Buy to Neutral. Goldmans had previously led a Blinkx stock placing of 45.68m shares at 120p at the time of their acquisition of Rhythm NewMedia in June 2013...

So Why Bother with Blinkx Now?

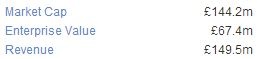

1. Valuation Is Appealing

Let's look at some simple valuation metrics:

Enterprise Value/Sales is 0.45x for a company that generated a 6.9% operating margin for FY2014:

Note the high net cash element of $126.9m, which highlights the company's solid balance sheet. This seems pretty cheap to me, at least on basic metrics.

Net free cashflow pre-acquisitions, post investments has been pretty solid too, averaging out at over $29m per year over FY2013 and FY2014, giving a free cash flow yield on enterprise value of 26%!

2. Insider Buying: The CEO Bought at 34p

Interestingly, as a show of faith in the company, the CEO Subhransu Mukherjee bought 250,000 shares at 34p immediately after the profit warning, with insiders now owning 2.11% of the company's shares..

3. The Company Now Has Authorisation to Buy Back Shares

Following the July 15 AGM, Blinkx (LON:BLNX) now has authorisation to buy back shares, which would be a better use of some of its net cash position than embarking on more acquisitions... This could at least provide a solid floor for the stock.

4. Change in US-Based Short Positions

According to this latest filing, US-based short positions as of mid-August are down to 5% of what they were at the end of April this year, representing just 0.02% of the outstanding share float.

What is more, major shareholder Blackrock (10.04% of the stock as of July 4) now refuse to lend out their Blinkx shares to short sellers, underlining their commitment to the stock.

BLINKX PLC ("BLNKF-0")

- OTC Short Positions on 2014/08/15 76,540 -2,315 0.52

Net Total Last Total Price Date Change Shorted Price Volume Range

2014/08/15 -2,315 76,540 0.52 49,200 0.50 - 0.59

2014/07/31 4,124 78,855 0.57 47,700 0.56 - 0.66

2014/07/15 2,025 74,731 0.63 576,600 0.53 - 1.10

2014/06/30 -838 72,706 1.07 98,100 1.00 - 1.15

2014/06/13 -1,900 73,544 - 46,700 1.06 - 1.19

2014/05/30 -136,672 75,444 - 30,500 1.24 - 1.37

2014/05/15 -1,272,791 212,116 1.24 178,000 1.08 - 1.62

2014/04/30 -516,692 1,484,907 1.48 56,800 1.35 - 1.48

2014/07/31 4,124 78,855 0.57 47,700 0.56 - 0.66

2014/07/15 2,025 74,731 0.63 576,600 0.53 - 1.10

2014/06/30 -838 72,706 1.07 98,100 1.00 - 1.15

2014/06/13 -1,900 73,544 - 46,700 1.06 - 1.19

2014/05/30 -136,672 75,444 - 30,500 1.24 - 1.37

2014/05/15 -1,272,791 212,116 1.24 178,000 1.08 - 1.62

2014/04/30 -516,692 1,484,907 1.48 56,800 1.35 - 1.48

* - Indicates that the closing price used is the last non-zero closing price and is not the closing price on the report date.

Summary: Still Very Risky, But Potentially Interesting Upside...

In short, blinkx has been the subject of a concerted short selling attack, has not helped itself by then following this with a profit warning, but now resides at an extremely attractive valuation level, IF you believe in the business model. Not a stock to put your granny's life savings into, certainly, but perhaps one worthy of consideration for a modest long position.

I personally am looking for an initial price target at around 50p. But more than ever with this stock, Do Your Own Research!

Edmund

Disclosure: I have bought some Blinkx (LON:BLNX) shares in my NISA.

- See more at: http://www.stockopedia.com/content/blinkx-and-you-may-miss-the-rebound-85674/#sthash.Jv4Yg0rP.dpufWednesday, 27 August 2014

Fairpoint plc: Ditch the Ethical Qualms, Buy It

Brief intro to Fairpoint (£FRP): from their own website

Brief intro to Fairpoint (£FRP): from their own website

Fairpoint is a consumer financial services business focused on serving financially stressed consumers. Our mission is 'Making money go further'.

Our business is structured into the following primary business lines in order to serve the needs of this consumer group:

- Individual Voluntary Arrangements (IVAs)

- Debt Management Plans (DMPs)

- Claims Management

Fairpoint's Key Brands

Reasons to Be Attracted to Fairpoint (LON:FRP)

While you may not approve of the types of debt management services that Fairpoint provide (e.g. there are free debt management services available to indebted individuals), there are a number of solid investment reasons underlying my enthusiasm for this £58m market cap small-cap stock:

- Valuation is attractive;

- Profitability and cash generation are impressive;

- Income return is good in this ZIRP environment with a 5% dividend yield;

- Stock price momentum is picking up, breaking resistance levels to the upside;

- Acquisition strategy is cautious and sensible, delivering growth at a decent price.

This is all summarised nicely in Fairpoint's UK StockRank:

Valuation: Cheap as Chips!

Whichever way you look at it, Fairpoint (LON:FRP) looks good value with a single-digit P/E and 9% free cash flow yield:

Income: a 5% Yield is not to be sniffed at!

Note not only that Fairpoint (LON:FRP) pays a 5% yield today, but that it is well covered at only a 40% payout ratio; not further that dividends have been steadily increased since they were initiated in 2010.

Growth: Double-Digit Top-Line Growth

Thanks in part to a prudent acquisition of law firm Simpson Millar, paid in part in shares via an earn-out (on targets set for June 2015 and June 2016), top-line growth should be double-digit both this year and next, driving sales from £28.4m at end-2013 to a forecast £36.1m by end-2015.

We can look at profit growth through the lens of the simplest 1-stage Gordon Growth Model, according to which, Fairpoint's internal growth rate is:

ROE x (1 - Payout Ratio)

= 11% x (1 - 40%) = 6.6%

This would in turn imply a long-term total return rate at around 12%, including the 5.1% dividend yield. But don't forget, Fairpoint's balance sheet is somewhat inefficient, with a net cash balance of £2.8m, which suggests that the underlying ex-cash ROE is closer to 13%, pushing the internal growth rate beyond 7%.

Profitability and Cash Generation: Very Solid

As the 96 Quality Rank implies, Fairpoint is high quality when running it by the numbers whether looking at profitability or cash flow:

Stock Momentum: Interesting Breakout

Fairpoint is breaking above a key horizontal resistance level of 135p; my first price target is thus 155p, the price gap that opened up on May 20. Beyond that, I am looking to around 231p, last seen in mid-2008 when business was strong (due to the weakening economy).

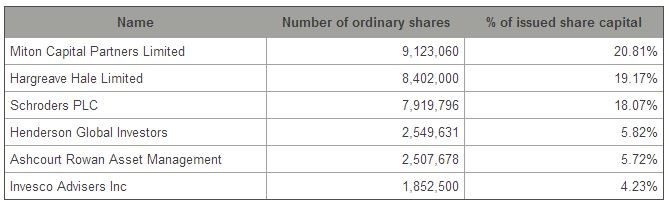

Stock Ownership: Extremely Concentrated Already

Another interesting feature of this stock is that stock ownership is extremely concentrated, making the stock vulnerable to an upwards stock squeeze in the event of any good news:

Three small-cap specialist fund management firms hold nearly 60% of the outstanding shares, including the top-ranked UK small-cap fund manager Gervais Williams at Miton (who runs The Diverse Income Trust plc amongst other funds - in which Fairpoint (LON:FRP) is the third-largest holding at 1.8% of the investment trust).

So any good news could see a big upwards squeeze in the shares in short order!

As always, please Do Your Own Research, however I have hopefully given you some points to chew over!

Disclosure: I hold Fairpoint shares in my SIPP

Edmund

Beware September; A Danger Month for Equities!

1. September Has Been The S&P’s Worst Month

2. Mid-September to Early October is Worst

3. Healthcare Does Best

4. Long Bonds Are Still A Good Place to Be

5. As Is Gold

6. Gold Stocks Get a Leveraged Boost

7. Natural Gas Tends To Be A Big Sept-Oct Winner: +22% in 2 Months on Average!

8. Total A Good Natural Gas Play

Summary

- Equity Markets Often Suffer in September

- Long Bonds Tend To See Lower Yields

- Sectors: Technology is Worst-Hit, Healthcare Does Best

- Two Commodities to Like In Sept-Oct: Gold, Natural Gas

- Two Stocks to Like: Goldcorp, Total

Friday, 22 August 2014

Global Strategy Weekly in Charts: Stocks to return to recent highs, then what?

Macro: Better US Outlook, But Europe Worrying

|

| 1. Markit Manufacturing PMI Points to Stronger US Recovery |

|

| 2. US Initial Jobless Claims Back to Cycle Lows |

|

| 3. Why the Fed Can Stay on Hold Longer: High 12.2% Under-Employment Rate |

|

| 4. German 10-year Bond Yield < 1% Higlights Deflation Risk: ECB to Help? |

Stock Markets: Tech, Financials Hit New High, Europe Rebounds

|

| 5. US Technology, Financials Sectors Break Out to New Highs |

|

| 6. German Stocks Lagged Word By Over 8%; Now Catch-Up Time |

Commodities: Has Crude Oil Found A Bottom At Last?

|

| 7. Brent Crude Oil Finally Bouncing Off $102/barrel |

|

| 8. Oil Services, Exploration/Production Start To Recover |

|

| 9. Nearly the Season for the Energy Sector To Perform! |

Risks: Watch For Mid-Term VIX to Return to <13

|

| 10. Mid-Term VIX Volatility Index Under 13 Will Flag Renewed Risk to Stocks |

|

| 11. Warning: US Retail Sentiment Back to Bullish High (Contrarian Signal) |

Investment Summary

- US Economic Recovery Seems to be Improving

- But High Under-Employment Means the Fed Can Wait…

- Risk-On Recovery Driving US Tech Financials To New Highs

- European Stocks Still Primed To Recover, But Hinges on the ECB

- Opportunity to Return to Oil Stocks As Brent Crude Bottoms

- Watch for the Mid-Term VIX to Dip Under 13; then risk/return may change

Edmund

Why Sandisk is a Top Technology Pick

This is an interesting turnaround, because several years ago I was in fact an actual bear of the stock due to its very high valuation. These days, I am a big fan of the company and the stock for 7 key reasons:

1. Well-Positioned Thematically

Sandisk is a key technology company exposed to some of my favourite long-term investment themes - The Internet of Things, the Mobile Internet and Big Data.2. Wide Moat

Sandisk is a leading NAND flash memory maker, the type of memory used in USB drives, smartphones, tablet computers and solid state hard drives. This type of storage is more expensive per gigabyte than a traditional mechanical hard drive (of the sort found in desktop PCs), but has the advantage of consuming far less power (important for mobile computing), having much fast data retrieval times and also being more robust (mechanical hard drives are typically very sensitive to shocks and extreme temperatures).Sandisk spends a heavy 12% of sales on Research & Development, which over time has led to the building of an extensive portfolio of valuable patents, which Sandisk monetises in the form of royalty payments received from other semiconductor makers who use their designs and technologies. This, combined with Sandisk's focus on higher-end NAND flash memory applications has allowed the company to maintain gross margins well north of 50%, over 10% better than their memory maker rivals such as Toshiba and Micron, and currently as high as 53%.

3. Strong Free Cash Flow

This high profit margin is converted in to bundles of cash, with between $1.4-1.6bn of net free cash flow generated per year over each of the last two years. With $4.2bn of net cash already on the balance sheet, this equates to a 8-10% free cash flow yield on Sandisk's enterprise value. Even with the drag of this cash pile on profitability, Sandisk is still achieving a Return on Equity not far shy of 15%.4. Valuation is attractive

An ex-cash 2015e P/E of under 12x and EV/EBIT ratio of 7.8x is cheap for such an innovative growth company, which is also paying a steadily rising dividend (1.1% yield) and which is also buying back shares (Sandisk is a member of the Powershares Buyback Achievers portfolio, for instance).5. Profit momentum is positive

Despite continued deflationary pressures in terms of $ per gigabyte of NAND flash storage, the drive to lower manufacturing costs and also the surge in volume demand is leading to upwards revisions to both sales and earnings forecasts (the company's consensus 2015e EPS forecast is over 10% higher today than it was at the start of 2014).6. Leading sell-side analysts are positive

The average consensus target price is $114 (vs. $97.55 now), while leading brokers such as Sanford Bernstein have a very bullish $150 target.7. Positive Technical Analysis

SanDisk (NSQ:SNDK) trades at $97.55 at present, while there is an upside price gap to fill on the share chart at $105.80, giving clear upside in the short-term. There is also a solid upwards price trend, in place since mid-2012.All in all, I see a good number of reasons to be a buyer of SanDisk (SNDK) today, although as always, you are advised to Do Your Own Research!

Edmund

See more at: http://www.stockopedia.com/content/why-sandisk-is-a-top-technology-pick-85555/#sthash.ciKy2SVf.dpuf

Subscribe to:

Posts (Atom)