- Some fund managers take a punt on small oil firms

- Expect bigger share price rebound with an oil recovery

- Focus on companies like Caza Oil, Bowleven, Soco

By Atul Prakash

LONDON, Feb 13 (Reuters) - After a rout in energy stocks on the back of a slump in crude oil prices, some fund managers have started fishing for smaller oil exploration companies, betting that a price recovery will lead them to outperform.

Smaller players, especially oil explorers, look much more attractive on valuation grounds than companies like BP BP.L and Royal Dutch Shell RDSa.L as their shares have fallen much more than oil majors during the sell-off, they said.

These stocks are not without risk -- unlike their more diversified and financially more robust bigger rivals, small firms are usually less able to offset a slump in oil prices. But investors say the potential rewards look attractive.

"I feel relatively confident that we have seen the bottom of the oil price. In such a scenario, high-beta (more volatile) plays like smaller oil explorers and service companies are the first to benefit," said Edmund Shing, global equity fund manager at BCS Asset Management.

"At these levels, they also become attractive M&A (takeover) targets as it may be cheaper for big companies to buy exploration firms than find new reserves. If oil prices gain, big players will become more confident, accumulate cash, cut capex and look for cheaper reserves."

Oil LCOc1 rose above $60 a barrel on Friday for the first time this year, with prices up more than 30 percent from a multi-year low in mid-January.

Shing said that in order to cut some risks, he was investing in firms having low debt and those which had hedged their future output. BCS recently bought Caza Oil & Gas CAZA.L , Bowleven BLVN.L , Soco International SIA.L , Eagle Rock Energy Partners EROC.O , Memorial Production Partners MEMP.O and Emerge Energy Services EMES.K .

Shares in the firms, except Memorial, are up 6 to 34 percent in the first two weeks of this month on a recovery in oil, which has gained 12 percent in February. In contrast oil majors like BP, BG Group and Shell are up 7 percent this month.

INDISCRIMINATE

Thomson Reuters data shows smaller oil firms are cheaper. Memorial trades at 14 times its 12 month forward earnings, while firms like Bowleven have a negative price-to-earnings ratio, against 30 times for BG Group and 20 times for BP. The 12-month price-to-book ratio for smaller oil firms hovers between 0.2 to 0.6, against 1.1-1.6 for large players.

"Smaller oil companies were hit by a slump in crude oil prices in an indiscriminate manner, so for some that was an over-reaction. It does make sense at this juncture to start

looking at them," said Chris Rowland, buy-side energy analyst at investment management company Ecofin.

"We like those smaller oil-related names that are operating in cheaper oil basins and are well-hedged, and without pressing near-term debt repayments or covenant tests, which is leading us to look to buy selected U.S. names at this stage."

Investment banks are also positive on some smaller oil firms, with Morgan Stanley recently raising its stance on Soco to "equal weight" from "underweight" and Exane BNP Paribas hiking its target price for the company. UBS, which has a "buy" rating for Memorial Production, has increased its target price for the stock to $18 from $15 the stock. ID:nWNAB05XO6

That is not to say that Big Oil is no longer attractive -- after all, majors have fought to protect their dividends by cutting spending -- but investors are looking at different ways to play a potential recovery.

"We are still positive on the oil sector, but have become very selective," James Butterfill, global equity strategist at Coutts.

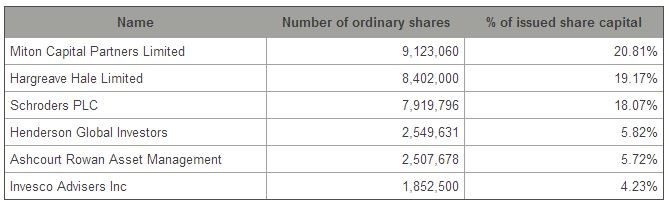

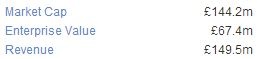

Brief intro to Fairpoint (£FRP): from their own website

Brief intro to Fairpoint (£FRP): from their own website