Showing posts with label Video. Show all posts

Showing posts with label Video. Show all posts

Wednesday, 14 October 2015

Thursday, 2 July 2015

Idle Investor: Three simple strategies to beat the professionals (VIDEO)

Video Interview with Juliet Mann of news.markets

In this first video of a new series, the Business Book Club, fund manager Edmund Shing explains his three simple strategies to earn high returns and beat the professionals.

Shing, global equity portfolio manager at BCS Asset Management in Paris, outlines his simple, low-risk investing system that beats market indices and fund manager performance over the long term, but requires only a few minutes of investors’ time each month.

The strategy is detailed in his book The Idle Investor and Shing argues that even the laziest investor can achieve it. The Idle Investor includes three straightforward DIY strategies for long-term investing, Shing tells Juliet Mann. All you have to do is follow the simple rules.

Each method requires only a limited amount of time and they all make use of easily accessible, low-cost funds. Shing’s three strategies are: The Bone Idle Strategy, The Summer Hibernation Strategy and the Multi-Asset Trending Strategy.

Yet, argues Shing, being idle doesn’t mean being unsuccessful. “If you are looking for a straightforward investing method that lets you get on with your life while your money grows in the background, then become an Idle Investor,” he says.

On CNBC Today Talking About China: A Long-Term Play, But Not Yet!

Be patient if investing in China: Fund manager

Edmund Shing, global equity portfolio manager at BCS Asset Management, discusses China's economy and its recent easing policies.

Thursday, 25 June 2015

Forget Greek debt woes and buy into the European market recovery

International Business Times UK Video link:

I have to admit it - I am sick of being asked over and over again for my opinion on Greece.

Will it stay in the Eurozone or will it be forced to leave? Is the Greek drachma going to come back? And so on and so on...

Here is what I really think deep down: whether Greece stays in the Eurozone or not, I believe that you should be investing in Eurozone stocks anyway.

I have three reasons for believing this:

1. The European economy is improving and Greece is small

Greece is the 13th-largest economy in the EU (out of 28 member states) and only contributes 1.3% to the EU by Gross Domestic Product (GDP), the classical measure of economic output.

So it frankly hardly moves the needle compared heavyweights such as the UK, Germany, France and Italy.

European economies are improving. Not just the UK's, which we can all see through the lens of the employment and property markets, but also in Continental Europe. In Germany, unemployment rates remain at generational lows. Wage growth is now starting to pick up, giving employees more purchasing power.

At the same time, the cost of living in the UK is staying low, thanks to the fall in oil and petrol prices plus subdued food prices. The cost of eating is being depressed in large part by ongoing price wars between supermarket chains and discounters like Aldi and Lidl.

Finally, the weaker euro has helped boost exports from Germany, Ireland and Spain to the rest of the world (while the strong pound is making the UK's exports relatively more expensive).

All of this has boosted the Euro zone's economic growth rate, as measured by GDP.

Eurozone GDP growth has picked up

Source: tradingeconomics.com

2. Reforms are boosting both economies and company profits

Ireland, Spain, Portugal, France and Italy have made varying degrees of progress in lifting regulations and easing job-market rules, changes that can lead to better growth. Ireland and Spain are now the fastest-growing economies in the EU, and even Portugal is improving.

At the company level, investors are seeing a whole host of reforms too. Companies have become much keener on cost-cutting and are targeting their investments on good growth prospects. It has become somewhat easier to hire and fire employees, an essential reform to encourage companies to employ more people to boost sales and profit growth in the long-term.

This corporate strength is reflected in the very high levels of business confidence seen across the European Union today, with companies looking to invest for future growth.

European business confidence is at a high

Source: tradingeconomics.com

The result is that the profitability of European companies has surged over the past few years. Even banks, which have been under the regulators' cosh since the 'Great Financial Crisis' are now starting to see growth in profits, which is translating into growth in dividends too.

3. European shares are cheap

At 15 times price/earnings ratio, the European stock market is cheap relative to other large stock markets such as the US. Shares in countries such as Spain and Italy look particularly cheap. And European stock markets are also cheap relative to their own history, if you compare today to the last 30 years.

At the same time, European companies pay out an average dividend yield of well over 3%, which is an income which is not to be sniffed at in these times of near-zero interest rates.

With the improvement in the underlying Euro economy continuing, European companies should continue to produce strong profit growth; thus an attractive combination of growth and value, which is what experienced investors look for.

What to buy? The direct way via an exchange-traded fund

The easy way to buy into European value and profit recovery is through a fund: I would recommend a cheap exchange-traded fund (ETF) such as the db x-trackers MSCI EMU Index UCITS ETF (code: XD5S).

This is an ETF that is:

- cheap (they only charge investors a management fee of 0.25% per year);

- priced in pounds sterling (current price £18.09); and

- currency-hedged so that investors do not suffer from any weakness of the euro currency against the pound sterling.

What to buy? The indirect way via UK stock which is heavily exposed to Europe

The second option is to buy shares in a UK company that has a heavy exposure to Continental Europe, and which should thus benefit from future Euro area growth.

I would look at Sky (code: SKY). We all know and love Sky for providing us with satellite TV (namely sports, movies and of course not-to-be-missed series such as Game of Thrones), but Sky has also recently integrated Sky Deutschland (its German + Austrian equivalent) and also Sky Italia (Sky in Italy).

In all three countries, Sky is the dominant satellite TV provider. Sky is an excellent company which is dominant in a number of the largest countries in Europe. It will thus benefit from higher consumer spending in Continental Europe.

As an additional inducement, remember that the Rupert Murdoch-controlled US-based Fox network still owns 39% of Sky's shares, and have recently rebuffed two offers to buy this Sky stake from Vodafone and from France's Vivendi.

Perhaps Murdoch is thinking of buying out the 61% of Sky's shares he doesn't own in the near future?

All in all, the bottom line is that Greek concerns should not dissuade you from investing in European recovery, whether via an exchange-traded fund or via Sky.

Tuesday, 16 June 2015

UK goes mad over online shopping - BooHoo and Sports Direct worth an investment look

I admit it – I just love buying stuff on Amazon. I love the simplicity, the speed, the ease; such a contrast to actually having to go out and find a shop on the high street that actually stocks what I want, and at a price I am prepared to pay!

Clearly, I am not alone.

The UK is gripped by online shopping fever

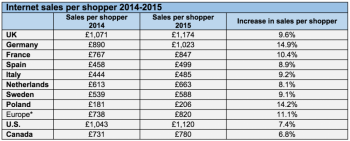

Today, almost £1 in every £8 is now spent online in the UK (Figure 1), by over 42 million digital shoppers. Now that is quite a feat, particularly when you realise that only 4% of all food sales are done online.

Online now represents more than £1 in every £6 spent on non-food sales, according to the British Retail Consortium.

1: Over 12% of total retail sales are done online

Source: ONS

As you might expect, online sales are growing faster than retail sales in "bricks and mortar" shops.

Online shopping grew 13% over the last year (to April 2015; Figure 2), compared with overall retail sales growth of under 5% since April 2014.

2: Online retail sales up 13% in a year

Source: ONS

UK is the European leader of internet shopping

Did you know that we in the UK are in fact the world leaders in internet shopping?

This year, we are predicted to spend nearly £1,200 shopping online, even more than the average American online shopper and around 10% more than in 2014 (Figure 3).

3: UK shoppers spend an average of £1,174 online

Source: econsultancy.com

Delving into the top 50 ecommerce retailers in the UK, 30 of them are from the retail sector, while another 12 are in travel, transportation and leisure.

Some of the top e-tailers are immediately obvious to anyone who has not been living in a proverbial cave: Amazon, Apple iTunes, and eBay.

Online shopping via mobile phones and tablets is now the fastest-growing area of ecommerce. And the top UK mobile retail category for searches is fashion, in the form of clothing, apparel and accessories. 65% of smartphone users search for fashion items using their device, according to Econsultancy (Figure 4).

4: Fashion is the most popular mobile retail search

Source: econsultancy.com

Investing in UK online retail

In the UK, BooHoo (code BOO), Asos (ASC) and Sports Direct (SPD) are all direct beneficiaries of this move to buying sports and fashion clothing online, at the cost of more traditional high street clothing chains such as BHS and TopShop.

Out of BooHoo, Asos and Sports Direct, I am particularly keen on BooHoo and Sports Direct as good long-term online retail plays.

A quick check on the Alexa web ranking website gives a very positive first impression (Figure 5). BooHoo.com is certainly getting more popular relative to other online retailers.

5. BooHoo.com is becoming more popular, relative to other similar websites

Source: Alexa.com

What is more, BooHoo's 10 June trading update highlighted a 35% increase in sales for the 3 months to 31 May, with 3.3 million active customers worldwide (32% more than a year ago).

Very strong growth, backed by lots of cash which can be used to make further investments for future growth too.

All in all, this looks a rather attractive proposition to me at BooHoo's current 28p share price.

Sports Direct harness Click and Collect

Sports Direct's website makes great use of their brick-and-mortar chain of stores to offer a "click and collect" service. With Click and Collect, you first order your sports goods on their website, and then collect the parcel from your chosen local Sports Direct store once it has arrived.

Online sales are now over 14% of Sport Direct's total sales, but are growing at an 11% annual clip and are also helping to improve the company's profitability.

While you pay £4.99 for this delivery option with Sports Direct, you get a £5 voucher back to spend in store when you collect your order. So while in principle you pay nothing for delivery, it cleverly entices you to make another purchase from either the store or the website.

Conclusion: BooHoo and Sports Direct are two great ways to invest in the UK online shopping boom.

Friday, 29 May 2015

Thursday, 28 May 2015

Make money from a strong pound at Marks and Spencer and Majestic Wines

IBTimes Video Link (click below):

This week, pound sterling hit its highest level against other major world currencies for over seven years (figure 1), judging by the Bank of England's Pound sterling index.

Figure 1: Trade-weighted pound back at highest since mid-2008

Source: Bank of England

This latest surge has been driven by the political certainty given by a Conservative general election victory, plus a following wind for the UK economy as:

- Unemployment continues to fall

- Retail sales surge higher (+4.7% year-on-year in April 2014)

- The domestic property market resumes its upwards march.

- Pound posts big gains against the euro and Aussie dollar

Of the major world currencies, the pound has gained against virtually all of them so far in 2015, save the Swiss Franc (figure 2).

Figure 2: Pound makes big gains against the euro and Australian dollar in 2015

Source: Bank of England

The biggest move has been the near 10% jump against the euro (from €1.29 at the beginning of 2015 to €1.41 currently).

The pound has also posted useful gains against the Australian dollar and Swedish crown too, with only the Swiss franc doing better this year so far.

Why should sterling stop here?

As long as the British economy keeps steaming along and the European Central Bank continues with its programme of bond buying (so-called Quantitative Easing, or QE), we could well see sterling return to the heady heights of €1.50 reached on several occasions between 2004 and 2007 (figure 3).

Figure 3: Pound hit over €1.50 several times 2004-07

Source: Bank of England

After all, the euro remains undermined by the ongoing Greek saga, while the extremist leftist party Podemos has made large gains in the local elections in Spain, underlining the political fragility of the established ruling parties across the eurozone and introducing yet further uncertainty.

Remember, if there is one thing financial markets hate, it is uncertainty – one area where the UK has a clear lead over its continental European cousins with a Conservative majority government now voted in.

How can we make money from a stronger pound?

One sector a canny investor should look at is the retail sector, given the majority of the goods sold on the UK high street tend to be imported. After all, a stronger pound means cheaper prices for imported goods, especially from the eurozone where the exchange rates have moved the most over recent months.

Food and drink is one big category where the UK imports a lot from the likes of Spain, France and Italy. Overall, the UK imports 40% of all the food consumed, much of it from our eurozone neighbours.

This should give a welcome boost to supermarket and upmarket food store chains such as Tesco (TSCO) and Sainsbury's (SBRY). I would focus more on two other retailers where I see potentially greater currency-related benefits.

The first is the venerable Marks and Spencer (MKS), which recently reported strong results. The retailer is continuing its slow transformation into primarily an upmarket food retailer along the lines of John Lewis's successful Waitrose chain.

Its Simply Food store format is enjoying a lot of success, and Marks and Spencer is focusing its new store programme on this format. While we may think fondly of the retailer as the nation's favourite purveyor of underwear, in actual fact food and drink now accounts for 57% of Marks and Spencer's UK sales.

The second retailer who could get a big profit boost from the stronger pound is wine warehouse chain Majestic Wines (MJW).

This £300m company is the UK's largest wine specialist merchant, with 213 stores selling wine by the case to 643,000 active customers.

French, Spanish, Italian and Australian wine imports in particular should all become cheaper in pound terms for Majestic to buy in the coming months and could deliver a useful profit bump.

Majestic should also see faster growth ahead following its recent acquisition of leading online business Naked Wines.

So go shopping for wine bargains thanks to that stronger pound, and why not add Marks and Spencer and Majestic Wines into your shopping basket while you are at it.

Tuesday, 19 May 2015

HSBC and Co-op Bank do battle as sub-1% mortgage wars break out

International Business Times Video Link below:

Could the first sub-1% mortgage rate be around the corner? Actually, it is already here. While the Co-op Bank recently launched a 1.09% two-year fixed-rate mortgage (which will move back to the standard variable rate (SVR) at the end of the term), HSBC has beaten this with an initial rate of 0.99% on its two-year discount special mortgage.

It is hardly surprising then that existing homeowners are thinking about remortgaging to lower their monthly mortgage payments. Surprisingly enough, the SVR on mortgages has actually risen since 2010 and now stands at 4.5%.

Figure 1. Two and five-year fixed mortgage rates still falling

Source: Bank of England

The average two-year fixed mortgage rate has fallen to under 2%, while the average five-year fixed rate is under 3% (Figure 1). And if you shop around, you can now find sub-2% five-year fixed rates too.

Nearly one in six homeowners are thinking about remortgaging over the next six months, according to a recent Nottingham Building Society survey.

They are hoping to save on average £99 per month, or nearly £1,200 per year. This is all thanks to the ongoing mortgage price war, driving rates ever lower. Let's face it, with the Bank of England base rate at a historic 0.5% low, interest rates are likely to only go one way in the long-term – up.

So remortgaging with a multi-year fixed rate will at least insulate the homeowner against the risk of higher rates for the foreseeable future.

Average mortgage rate on outstanding mortgages

But how much is the average mortgage borrower paying at the moment? The Bank of England says "nearly 3.2%" (Figure 2).

Yes, this average rate has come down over the past five years, but it is still a long way from the current best two and five-year fixed and discount rates on offer today.

Figure 2. Average mortgage rate on outstanding mortgages still over 3%

Source: Bank of England

Let's say you are interested in remortgaging your house or flat. Where would you start and what should you watch out for?

Firstly, you can go the well-trodden route of checking out the online mortgage best buy tables at MoneySuperMarket.com, MoneySavingExpert.com or MoneyFacts.

Before going any further, it is probably a good idea to sit down with your existing mortgage provider to see what they can offer you.

Then if you're not satisfied, try the banks and building societies at the top of these tables. Or you could go to a specialist mortgage broker such as John Charcol or London & Country Mortgages.

But beware, some of these lowest interest rates come with catches: you may be hit with a high "arrangement fee" that can go as high as £1,499, or there may be penalties for early repayment. So be careful to examine the details.

Investing in the mortgage market: challenger banks, specialist lenders

There are some interesting ways to invest in a post-election pick-up in mortgage demand. Instead of looking at the Big Four UK banks, I would look to the new "challenger" banks that have recently been established, or look to specialist mortgage lenders.

Listed challenger banks that are making a splash on the savings and loans markets include Virgin Money (code VM.), Secure Trust Bank (STB), OneSavings Bank (OSB) or Aldermore Group (ALD).

Virgin, OneSavings and Aldermore have all recently listed on the London Stock Exchange and are growing their savings and mortgage businesses quickly as they take business away from the Big Four.

Otherwise, for a really focused mortgage growth play, you could look at the Paragon Group of Companies (code PAG). Paragon specialises in residential mortgages (such as buy-to-let), personal and car loans.

They are forecast to grow profits by more than 10% per year for the next two years and trade on a very reasonable valuation.

Bottom line: if you haven't remortgaged already recently, check out the current best remortgage buys and see if you can save on your monthly payments.

Thursday, 14 May 2015

CNBC TV Interview: Bonds - Expect more extreme moves

Edmund Shing, global equity portfolio manager at BCS Financial Group, says bond volatility is on the up.

Click on link below to watch the video clip:

Wednesday, 13 May 2015

On Bloomberg TV: Discussing the Economy

BCS Asset Management’s Edmund Shing and Mizuho International’s Riccardo Barbieri discuss Greece’s ongoing talks with its creditors and an IMF payment that the country made. They speak to Bloomberg’s Jonathan Ferro on “On The Move.” (Source: Bloomberg)

Bloomberg TV link:

Tuesday, 12 May 2015

Goodbye Labour mansion tax, hello Tory post-election property bonanza at Berkeley and Foxtons

International Business Times Video link (click below):

Could property be the big gainer from David Cameron's election win? Estate agent Foxtons and house builder Berkeley Group jumped 9%+ on 8 May. But why?

Clearly, the stock market has heaved a huge sigh of relief at the demise of the Labour Party. Now there is no fear of a mansion tax hitting London housing.

This is good news for house buyers at the £2m ($3m, €2.7m) plus price bracket, such as foreign buyers in London, who have been holding off any purchases up until now.

Equally well, with the risk of Labour's threatened rent controls now removed, the buy-to-let market could now see renewed activity.

Now that the Tories are in sole charge, they need to urgently tackle one of Britain's most pressing problems. London and the South East is the UK's economic heartbeat, but is desperately short of affordable housing.

House prices still on the rise – outside London

The Halifax house price index rose 1.6% between March and April, and 8.5% over the last year, for a yearly gain of nearly £20,000 on the average house (Figure 1).

Figure 1: UK house prices up by nearly £20,000 over the last year

Source: Lloyds Bank

Last year, London properties saw the fastest-rising prices. In contrast, it is the rest of the UK that has enjoyed stronger house price momentum over these last 3 months.

According to the Royal Institute of Charted Surveyors (RICS), London is one of the very few regions where house prices have actually fallen over the last 3 months (Figure 2).

Figure 2: House prices rising fastest in Northern Ireland

Source: Royal Institute of Chartered Surveyors

Four factors should drive a rebound in buy-to-let house purchases:

- Lifting of the threat of rent controls;

- High demand for rental properties (Figure 3);

- Falling mortgage interest rates: The Co-Op Bank are now offering a new 2-year fixed-rate mortgage at only 1.09%. This suggests that the first sub-1% mortgage rate could soon be here.

- Falling savings rates: your saved cash is worth less and less in the bank, increasing the attractions of alternative income investments.

Figure 3: National rental demand remains very high

Source: Royal Institute of Chartered Surveyors

All good for estate agents and house builders

What are the best ways to invest in the UK housing market? These are my two favourite housing-related industries:

Estate agents: Of course they buy and sell houses, and so make more money as house prices go up. But they also increasingly make money from the buy-to-let market, as they also act as letting agents.

House builders: who benefit from rising house prices as they can sell their newly-built homes for more, meaning higher profits.

My two favourite housing shares: Berkeley Group and LSL

I like the UK house builders as a group; they are all in general cheap, pay big dividends and are very profitable.

My favourite house builder is Berkeley Group (code BKG). It is focused on London and the South East of England, it is a generous income payer with a 6.4% dividend yield, and has been consistently very profitable over the last five years.

There are handful of listed estate agents in the UK. I like LSL Property Services (code LSL). LSL has two distinct sets of businesses:

- 539 estate agent branches under a number of brands, such as Your Move and Reeds Rains;

- Surveying and valuation services.

Both of these sets of businesses will make more money from a booming property market, whether from buying and selling or just from managing rented properties.

LSL is also a cheap stock and a reasonable income payer with a 3.7% yield; it is also consistently very profitable, with profits forecast to grow by 10% this year.

Post-election Friday was a good day for the estate agents and house builders; but there could be many more as the property market heats up again!

Thursday, 23 April 2015

Bloomberg TV interview this morning - discussing China, Greece...

BCS Asset Management Global Equity Portfolio Manager Edmund Shing discusses

-

He speaks to Bloomberg’s Mark Barton, Caroline Hyde and Manus Cranny on “Countdown.” (Source: Bloomberg)

- China’s Flash PMI data,

- Greece’s debt deal and

- where he sees opportunity.

-

He speaks to Bloomberg’s Mark Barton, Caroline Hyde and Manus Cranny on “Countdown.” (Source: Bloomberg)

Bloomberg TV Video Link Below:

Wednesday, 22 April 2015

CNBC Squawkbox Guest Host: Video on Chinese, Hong Kong Equities Value

Edmund Shing, global equity portfolio manager of BCS Financial Group, says he still sees value in the Hong Kong and Chinese stock markets.

Please click below to view the VIDEO Link:

Tuesday, 21 April 2015

Grexit Today, Brexit Tomorrow?

IB Times Video Link (click on link below to view):

Is the Greek government really preparing to leave the Eurozone and re-introduce the Drachma? Another week goes by, and still no deal between the Greek government and the European Union (EU), European Central Bank (ECB) and the International Monetary Fund (IMF). Time is running out for the Greeks to secure the financing from these negotiating parties that they require to avoid defaulting on their government bonds.

But what is “Defaulting”, and why does it matter?

Defaulting simply means that the Greek government refuses to pay the contractual interest on borrowing it has previously taken out in the form of government bonds (which are simply IOUs to the eventual bond buyers). In addition, it means that the Greek government also refuses to repay the capital for loans that have arrived at maturity, meaning that the bond buyers who have previously lent their money to the Greek government will not get all of the original amount lent out back.

This type of borrowing is quite unlike a capital repayment mortgage, where we take out a mortgage secured on a house for a fixed period of time e.g. 25 years. With such a mortgage, we are effectively repaying the lender (a bank or building society) a mixture of interest payment and capital repayment month by month, such that the entire original amount borrowed is repaid by the end of the life of the mortgage.

And if we don’t make our monthly payments on time, the lender has the right eventually to repossess our house and resell it in order to recoup their original capital lent out plus interest payments due – i.e. “secured” lending.

Contrast this to the government bond type of borrowing, where a sovereign government issues IOUs in the form of selling bonds, promising to pay a set amount of interest every year until the end of life of the bond (e.g. 10 years), at which point they then have to repay the entire amount originally borrowed in one lump sum back to the lenders (the bond holders).

If, however, a country defaults by not paying the agreed interest payments on time or not repaying the original capital at the end of life of a bond, there is (generally) no asset that the original lender can seize to resell to recoup their capital and interest – it is “unsecured” lending.

By not putting forward the essential economic reforms that the EU, the ECB and IMF are demanding in return for extending further loans to the Greek government, the Greek Prime Minister Alexis Tsipras risks telling holders of Greek bonds that they will not get their interest payments and their capital lump sums back, as the Greek government coffers are already almost empty.

This would not be the first time that a Greek government defaults on its debts – in fact, in the modern era Greece has defaulted five times (since 1826; Figure 1).

1. Five Greek Debt Defaults Already in the Modern Era

Source: Forbes

Source: Forbes

How Much Longer Can The Greeks Struggle On Before Default and Grexit?

So, the Greek government has already run out of money; it has been struggling on up to now by raiding whatever pots of cash it has been able to get its hand on in the very short-term. But as Figure 2 shows, a big set of debt repayments are due in June, and an even larger amount of repayments come due in July.

2. Upcoming Greek Government Debt Repayment Schedule

Source: IMF, Datastream

Source: IMF, Datastream

Without a reform deal acceptable to the EU, ECB and IMF, the Tsipras-led administration almost certainly has to decide either to default either by:

- not repaying bond holders (the largest of which are actually other Eurozone governments, the ECB and the IMF; Figure 3) or by

- not paying its own citizens their pensions and state benefits.

3. Major Owners of Greek Debt

Source: Der Spiegel, portfolioticker.com

What Might This Mean for the European Union; What Chance of Brexit too?

While the Greeks might be able to struggle on despite a default, and stay in theory part of the Eurozone, in practice they would be forced to exit the Eurozone in short order, the so-called “Grexit”. Frankly, this could prove chaotic for financial markets as no-one really knows how a Eurozone member can exit the single monetary union (it was never legislated for when the euro was created).

This could also have some serious knock-on effects for British membership of the European Union, as a Grexit could prove a serious blow to the reputation of the EU in the UK, adding grist to the mill of UKIP and the Eurosceptic wing of the Conservative Party.

A Greek exit from the Eurozone could effectively increase the chance that Britain leaves the European Union in a post-election referendum, which in turn could prove a massive problem for those UK companies doing a lot of their business with our European Union partners like Germany and France – the European Union as a block remains the UK’s largest trading partner by far at 51% of UK exports (Figure 4)…

4. Who the UK Trades With

Source: HMRC (2012)

Source: HMRC (2012)

One potential consequence could be the flight of companies to set up their head offices and operations in the Republic of Ireland, which would then become even more attractive as a business destination for several reasons:

• It uses the euro as its trading currency,

• It offers a low 12.5% corporate tax rate for overseas companies; and

• Good access to a (cheaper thanks to a weaker euro) skilled workforce plus easy transport access.

Conclusions: A Body Blow for the UK Economy?

Failure for the Greek government to reach a last-minute deal with the EU, ECB and IMF is becoming ever more likely day by day. This could trigger a chaotic Greek exit from the Euro, leading volatility to surge in the financial markets.

Any subsequent post-election British exit from the European Union risks the loss of Europe-linked jobs in export-oriented sectors such as the car industry, and would potentially also be a body blow for the City of London, which a massive invisible export earner for the UK – opening the door for Frankfurt to challenge London once again for the crown of Europe’s pre-eminent financial centre.

Buy Into Irish Stocks

How can you profit from the Grexit + Brexit risks? By buying into major Irish stocks that could stand to benefit from any flight of UK companies to Dublin: I like Smurfit Kappa (code: SKG), Ryanair (code: RYA) and Hibernia REIT (code: HBRN).

Edmund

Is the Greek government really preparing to leave the Eurozone and re-introduce the Drachma? Another week goes by, and still no deal between the Greek government and the European Union (EU), European Central Bank (ECB) and the International Monetary Fund (IMF). Time is running out for the Greeks to secure the financing from these negotiating parties that they require to avoid defaulting on their government bonds.

But what is “Defaulting”, and why does it matter?

Defaulting simply means that the Greek government refuses to pay the contractual interest on borrowing it has previously taken out in the form of government bonds (which are simply IOUs to the eventual bond buyers). In addition, it means that the Greek government also refuses to repay the capital for loans that have arrived at maturity, meaning that the bond buyers who have previously lent their money to the Greek government will not get all of the original amount lent out back.

This type of borrowing is quite unlike a capital repayment mortgage, where we take out a mortgage secured on a house for a fixed period of time e.g. 25 years. With such a mortgage, we are effectively repaying the lender (a bank or building society) a mixture of interest payment and capital repayment month by month, such that the entire original amount borrowed is repaid by the end of the life of the mortgage.

And if we don’t make our monthly payments on time, the lender has the right eventually to repossess our house and resell it in order to recoup their original capital lent out plus interest payments due – i.e. “secured” lending.

Contrast this to the government bond type of borrowing, where a sovereign government issues IOUs in the form of selling bonds, promising to pay a set amount of interest every year until the end of life of the bond (e.g. 10 years), at which point they then have to repay the entire amount originally borrowed in one lump sum back to the lenders (the bond holders).

If, however, a country defaults by not paying the agreed interest payments on time or not repaying the original capital at the end of life of a bond, there is (generally) no asset that the original lender can seize to resell to recoup their capital and interest – it is “unsecured” lending.

By not putting forward the essential economic reforms that the EU, the ECB and IMF are demanding in return for extending further loans to the Greek government, the Greek Prime Minister Alexis Tsipras risks telling holders of Greek bonds that they will not get their interest payments and their capital lump sums back, as the Greek government coffers are already almost empty.

This would not be the first time that a Greek government defaults on its debts – in fact, in the modern era Greece has defaulted five times (since 1826; Figure 1).

1. Five Greek Debt Defaults Already in the Modern Era

Source: Forbes

How Much Longer Can The Greeks Struggle On Before Default and Grexit?

So, the Greek government has already run out of money; it has been struggling on up to now by raiding whatever pots of cash it has been able to get its hand on in the very short-term. But as Figure 2 shows, a big set of debt repayments are due in June, and an even larger amount of repayments come due in July.

2. Upcoming Greek Government Debt Repayment Schedule

Source: IMF, Datastream

Without a reform deal acceptable to the EU, ECB and IMF, the Tsipras-led administration almost certainly has to decide either to default either by:

- not repaying bond holders (the largest of which are actually other Eurozone governments, the ECB and the IMF; Figure 3) or by

- not paying its own citizens their pensions and state benefits.

3. Major Owners of Greek Debt

Source: Der Spiegel, portfolioticker.com

What Might This Mean for the European Union; What Chance of Brexit too?

While the Greeks might be able to struggle on despite a default, and stay in theory part of the Eurozone, in practice they would be forced to exit the Eurozone in short order, the so-called “Grexit”. Frankly, this could prove chaotic for financial markets as no-one really knows how a Eurozone member can exit the single monetary union (it was never legislated for when the euro was created).

This could also have some serious knock-on effects for British membership of the European Union, as a Grexit could prove a serious blow to the reputation of the EU in the UK, adding grist to the mill of UKIP and the Eurosceptic wing of the Conservative Party.

A Greek exit from the Eurozone could effectively increase the chance that Britain leaves the European Union in a post-election referendum, which in turn could prove a massive problem for those UK companies doing a lot of their business with our European Union partners like Germany and France – the European Union as a block remains the UK’s largest trading partner by far at 51% of UK exports (Figure 4)…

4. Who the UK Trades With

Source: HMRC (2012)

One potential consequence could be the flight of companies to set up their head offices and operations in the Republic of Ireland, which would then become even more attractive as a business destination for several reasons:

• It uses the euro as its trading currency,

• It offers a low 12.5% corporate tax rate for overseas companies; and

• Good access to a (cheaper thanks to a weaker euro) skilled workforce plus easy transport access.

Conclusions: A Body Blow for the UK Economy?

Failure for the Greek government to reach a last-minute deal with the EU, ECB and IMF is becoming ever more likely day by day. This could trigger a chaotic Greek exit from the Euro, leading volatility to surge in the financial markets.

Any subsequent post-election British exit from the European Union risks the loss of Europe-linked jobs in export-oriented sectors such as the car industry, and would potentially also be a body blow for the City of London, which a massive invisible export earner for the UK – opening the door for Frankfurt to challenge London once again for the crown of Europe’s pre-eminent financial centre.

Buy Into Irish Stocks

How can you profit from the Grexit + Brexit risks? By buying into major Irish stocks that could stand to benefit from any flight of UK companies to Dublin: I like Smurfit Kappa (code: SKG), Ryanair (code: RYA) and Hibernia REIT (code: HBRN).

Edmund

Wednesday, 15 April 2015

Oil Takeover Targets – Who’s Next?

Has a rush to buy up oil & gas companies just started? Royal Dutch Shell is set to become by far the largest FTSE 100 member by market capitalisation at 7.6% of the index (Figure 1), worth nearly £160 billion and 35% larger than the second-largest company HSBC, once it completes the £47 billion purchase of BG later this year.

1. Royal Dutch Shell Worth 7.6% of FTSE 100 Post BG Deal

Source: Author, stockopedia.com

In the late 1990s, the oil price plunged to $10 per barrel and set off a wave of oil industry mega-mergers: Exxon with Mobil, Chevron with Texaco, BP with Amoco. Fast forward to April 2015, and once again the oil price has plunged, more than halving from $110 per barrel in July last year to just $50 by January this year.

Now we have a new oil & gas mega-merger, Royal Dutch Shell taking over BG (the gas-dominated exploration and production arm of the former British Gas). This is in fact the second big oil company merger announced in the past few months, following US oil services company Halliburton which announced a merger with rival Baker Hughes in November last year.

Why is Shell Buying BG?

With this purchase of BG, which has been beset by fundamental problems for some time, Shell is buying access to oil and gas reserves in Brazil and Liquefied Natural Gas (LNG) capability. These assets allow Shell to grow their oil & gas reserve base (replacing oil and gas currently being produced) and to be a dominant player in the growing LNG market, alongside the state of Qatar.

The basic idea is this: that the oil & gas-producing assets of BG are cheaper for Shell to buy in principle than developing new oil & gas fields and putting them into production – the so-called “replacement” cost. Why take the risk of developing new oil fields (which may not even produce as expected), when you can buy proven, producing oil & gas reserves off the shelf?

Who Else Could Be Looking To Buy Oil & Gas Assets?

While Shell has already chosen its prey, which other mega-oil companies could also be looking to buy up cheap oil & gas reserves? As the oil & gas market is global by nature, we have to look abroad for potential acquirers.

In the US, ExxonMobil and ChevronTexaco are the two largest integrated oil companies with the financial muscle to do big deals. In Europe, Total of France and Statoil of Norway stand out as huge integrated oil companies that might find it easier and cheaper to buy up oil & gas reserves via acquisition of companies rather than by developing new oil & gas fields from scratch.

Who could be next to succumb to oil merger mania? BP?

In the UK, there are both big and smaller potential acquisition targets in the Oil & Gas sector. In a previous IBT article I have highlighted the attractions of the ailing BP (hurt by the 2010 Gulf of Mexico Macondo disaster).

BP could be an interesting target for the two US mega-oil companies Exxon and Chevron, given its huge asset base in the US/Alaska. I should note that BP has gained over 10% since I discussed it back in December last year, and BP’s market size is only 35% that of Exxon and 63% that of Chevron (Figure 2)…

2. BP Could Be a Target For US Giants Exxon, Chevron

Source: Bloomberg.com

Other Potential UK-Based Targets: Tullow, Premier Oil, EnQuest, Ithaca Energy

Otherwise, the oil exploration & production companies Tullow Oil (total company value: £5.2 billion; code TLW) and Premier Oil (total company value: £2.2 billion; code PMO) have both been cited as potential acquisition targets, and look cheap when comparing their total company value (the value of all shares + value of debt) to the number of barrels of oil they hold as Proven + Probable (2P) reserves in their developed oil fields (Figure 3).

For instance, Premier Oil is currently valued at just $13 per barrel of 2P oil reserves following a drop of more than 50% in its share price from September 2014 to now (from 348p to 159p). Could an integrated oil giant swoop to acquire these now-cheap oil reserves?

3. Four Small/Mid-Cap Oil Targets? Valued at $10-22 Per Barrel of Oil Reserves

Source: Author, Company reports

Both Tullow Oil and Premier Oil have global oil & gas interests, spanning from West and North Africa to Pakistan and the Falkland Islands.

Closer to home, other acquisition targets could include the smaller, North Sea-focused oil exploration and production companies EnQuest (code ENQ, current share price 42p) and Ithaca Energy (code IAE; current share price 46.5p). Both of these companies also look like potentially cheap acquisitions for larger oil company predators, at values of only $6 and $14 respectively per barrel of oil held in their various North Sea oil fields, and benefit from the reduction in North Sea oil taxes in the latest UK Budget.

There you have it: five UK-listed oil companies of varying sizes that could become tasty acquisition targets for global oil companies!

Edmund

Thursday, 9 April 2015

CNBC TV: Greek reforms - The risks ahead

From my recent Guest Host spot on CNBC's Closing Bell with Louisa Bojesen:

Edmund Shing, global equity portfolio manager at BCS Financial Group, discusses Greece's reform plans and the potential risks ahead.

Edmund Shing, global equity portfolio manager at BCS Financial Group, discusses Greece's reform plans and the potential risks ahead.

Video Link below:

Wednesday, 8 April 2015

Idris Elba gives Superdry the premium touch as Debenhams enjoys its sweet spot

International Business Times Video Link below:

We as a nation spent £26.5bn (€36bn, $39bn) in the shops during February, ie £6.6bn per week. The latest retail sales data reveals we bought 5.7% more stuff from shops in the second month of the year than in 2014, an impressive growth rate.

Clearly the combination of increasing employment, rising wages and lower petrol prices are driving greater consumer optimism and are all leading us to open up our wallets and spend with abandon...

A schizophrenic retail sector: Supermarkets pressured, non-food flies

Looking under the hood of retail sales statistics reveals two very different trends at work: firstly, supermarkets continue to have a tough time, with sales flat and prices under pressure (food prices on average 2% lower now than this time in 2014).

Secondly, in sharp contrast, the non-food retail sector is enjoying a boom (Figure 1), with a 5.3% increase in retail sales value over a year ago.

Figure 1. A tale of two sectors: Food retail flat, non-food booms

Source: Office for National Statistics

Digging deeper, the sectors producing the best growth at the moment are clothing, electrical appliances and household goods (furniture, lighting, Figure 2), all growing at over 6% per year.

Figure 2. Clothing, electrical and household goods in the lead

Source: Office for National Statistics. Data as of February 2015

In the UK retail space, the obvious names come to mind such as the veritable Marks & Spencer, Next and even Whitbread (the owner of Costa Coffee, Beefeater Grill and Brewers Fayre).

So which companies should be making hay? Debenhams and SuperGroup

But I would focus right now on two other retail names: department store chain Debenhams and the owners of the popular Superdry fashion brand, SuperGroup.

I like Debenhams (code: DEB) for a number of reasons:

- It sits in the current sweet spot of retailing, offering clothing, footwear and household goods in its department stores.

- Current trading is strong, following the strong key Christmas period with 4.9% like-for-like sales growth. Online was strong too with its debenhams.com website growing sales by 29% over the four-week period, helped by the success of its click-and-collect service.

- Gross profit margins continue to improve, highlighting the better cost control and fewer discounted items sold.

- Valuation remains cheap at only 10x P/E (thus far cheaper than Next, Marks & Spencer or Associated British Foods – owner of Primark; Figure 3), while income lovers will like the 4.6% dividend yield paid out.

Figure 3. Debenhams, SuperGroup cheaper than other UK retailers

Source: Stockopedia.com. Note: SuperGroup P/E adjusted for net cash

The stock has been on a strong run of late, rising from under 60p in October 2014 to touch a peak at the end of February of over 80p, before settling back to 76p now. I think there could be plenty more upside left in Debenhams, given the following winds from the UK economy.

SuperGroup: Buying into the new strategy

SuperGroup (code SGP), the retailer behind Superdry, has decided to buy back the distribution rights for its fashion brand in the US, so as to sell Superdry clothing Stateside rather than through a partner. At the moment, Superdry is not making money in the US, but this strategic move highlights the new management's confidence in its US growth potential.

Secondly, it has recruited actor Idris Elba (The Wire, Luther, Prometheus, Pacific Rim, Thor) for a collaboration on a new premium range of Superdry clothing, which should deliver a boost to UK sales.

Thirdly, it is initiating a dividend for the first time, which will allow part of the £66m of cash on its balance sheet to be progressively returned to shareholders.

Top-line growth for Superdry is still estimated to beat 10% per year going forwards, generating 12-14% earnings growth. For this, an investor is paying just over 13x P/E on an ex-cash basis, which seems a remarkably good deal for this recovering branded goods growth story. So shop till you drop with Debenhams and SuperGroup.

Subscribe to:

Posts (Atom)