I admit it – I just love buying stuff on Amazon. I love the simplicity, the speed, the ease; such a contrast to actually having to go out and find a shop on the high street that actually stocks what I want, and at a price I am prepared to pay!

Clearly, I am not alone.

The UK is gripped by online shopping fever

Today, almost £1 in every £8 is now spent online in the UK (Figure 1), by over 42 million digital shoppers. Now that is quite a feat, particularly when you realise that only 4% of all food sales are done online.

Online now represents more than £1 in every £6 spent on non-food sales, according to the British Retail Consortium.

1: Over 12% of total retail sales are done online

Source: ONS

As you might expect, online sales are growing faster than retail sales in "bricks and mortar" shops.

Online shopping grew 13% over the last year (to April 2015; Figure 2), compared with overall retail sales growth of under 5% since April 2014.

2: Online retail sales up 13% in a year

Source: ONS

UK is the European leader of internet shopping

Did you know that we in the UK are in fact the world leaders in internet shopping?

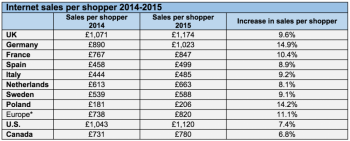

This year, we are predicted to spend nearly £1,200 shopping online, even more than the average American online shopper and around 10% more than in 2014 (Figure 3).

3: UK shoppers spend an average of £1,174 online

Source: econsultancy.com

Delving into the top 50 ecommerce retailers in the UK, 30 of them are from the retail sector, while another 12 are in travel, transportation and leisure.

Some of the top e-tailers are immediately obvious to anyone who has not been living in a proverbial cave: Amazon, Apple iTunes, and eBay.

Online shopping via mobile phones and tablets is now the fastest-growing area of ecommerce. And the top UK mobile retail category for searches is fashion, in the form of clothing, apparel and accessories. 65% of smartphone users search for fashion items using their device, according to Econsultancy (Figure 4).

4: Fashion is the most popular mobile retail search

Source: econsultancy.com

Investing in UK online retail

In the UK, BooHoo (code BOO), Asos (ASC) and Sports Direct (SPD) are all direct beneficiaries of this move to buying sports and fashion clothing online, at the cost of more traditional high street clothing chains such as BHS and TopShop.

Out of BooHoo, Asos and Sports Direct, I am particularly keen on BooHoo and Sports Direct as good long-term online retail plays.

A quick check on the Alexa web ranking website gives a very positive first impression (Figure 5). BooHoo.com is certainly getting more popular relative to other online retailers.

5. BooHoo.com is becoming more popular, relative to other similar websites

Source: Alexa.com

What is more, BooHoo's 10 June trading update highlighted a 35% increase in sales for the 3 months to 31 May, with 3.3 million active customers worldwide (32% more than a year ago).

Very strong growth, backed by lots of cash which can be used to make further investments for future growth too.

All in all, this looks a rather attractive proposition to me at BooHoo's current 28p share price.

Sports Direct harness Click and Collect

Sports Direct's website makes great use of their brick-and-mortar chain of stores to offer a "click and collect" service. With Click and Collect, you first order your sports goods on their website, and then collect the parcel from your chosen local Sports Direct store once it has arrived.

Online sales are now over 14% of Sport Direct's total sales, but are growing at an 11% annual clip and are also helping to improve the company's profitability.

While you pay £4.99 for this delivery option with Sports Direct, you get a £5 voucher back to spend in store when you collect your order. So while in principle you pay nothing for delivery, it cleverly entices you to make another purchase from either the store or the website.

Conclusion: BooHoo and Sports Direct are two great ways to invest in the UK online shopping boom.